Don’t get burned this summer by liability risks

Eager to get that grill fired up and invite your friends over for a backyard barbecue? Before stocking up on charcoal, lighter fluid, and groceries, it’s a good idea to take stock of your homeowners insurance. That’s because risks increase dramatically around homes during the warmer summer months. After all, it's a time when many of us host more guests and outdoor activities that can involve pools, trampolines, fire pits, and other alfresco amenities that can cause

Before you take a bite of that grilled bratwurst, chew on this: Of the roughly 140 million emergency room visits every year, roughly .

takes a closer look at common summertime liability hazards, how liability coverage in your homeowners policy can help, and strategies for decreasing your susceptibility.

Common Summer Liability Risks Around the Home

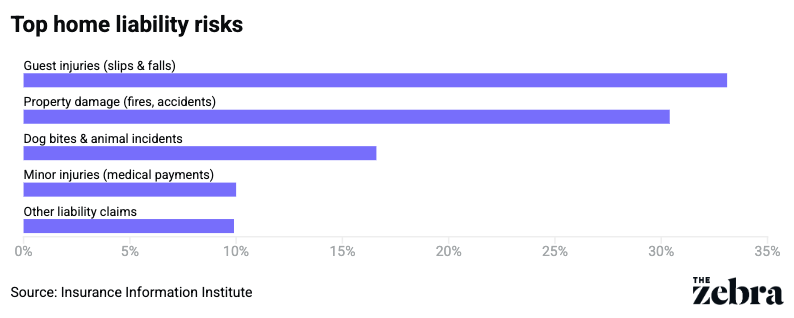

Decks, hot tubs, grills, playsets, and other backyard staples are synonymous with outdoor enjoyment during the warmer months, but they also increase the likelihood of someone getting hurt and you getting sued.

“From an insurance perspective, you can be held responsible if someone is injured or a guest’s property is damaged on your property, even if it was an accident,” explains , insurance analyst for The Zebra. “Outdoor spaces tend to come with a different kind of risk than indoor ones. You’ve got wet surfaces, open flames, uneven walkways, stairs, pets, play equipment, and all the little things that can turn into a bigger issue if someone gets injured. And the more people there are using your yard and outdoor areas, the more opportunities there are for something to go wrong.”

Pools and hot tubs

, director of strategic communication for the Insurance Information Institute, cautions that hot tubs and pools are among your highest liability exposures “because drowning, slips and diving injuries can be severe and costly, especially when proper fencing, covers or supervision are lacking.”

These are among the reasons why carriers prefer that you have safety measures in place, like fences, gates, or covers, which your municipality may also require.

Trampolines and playsets

Backyard play structures, inflatables, and trampolines are other common contributors to serious injuries to kids, which is why many insurers consider them that could impact what they will cover.

“Trampolines in particular cause a lot of injuries. Your policy may even exclude coverage on it, which you might not know until you need to file a claim,” says , a personal injury lawyer.

Backyard parties and guest injuries

Truth is, when you host more human beings in your yard and home, there’s more opportunity for unintended harm, and when alcohol plays a part, impaired judgment and physical violence.

“I’ve been involved in these types of cases where, for example, a guest slipped on a wet deck or got injured because of the negligent activities of another guest, and the homeowners had no idea that their insurance would not cover it,” says attorney .

Grills, fire pits, and outdoor entertaining

Flames and extreme heat in close proximity to human beings can be a dangerous combination.

“Fire pits and grills can lead to burns, fires, or property damage if used improperly, left unattended, or placed too close to structures or vegetation,” Ruiz adds.

Dogs and other pets

Even a friendly pooch can get overwhelmed by unfamiliar guests, noise, or children.

“I’ve been encountering cases lately in which a dog that had never exhibited aggression before bit a guest at a backyard barbecue, and the owner had to confront a civil claim that their homeowners policy would not cover in full,” notes Kruse.

How Home Liability Coverage Helps

Backyard leisure amenities like a pool, cold plunge tub, deck, playset, and outdoor kitchen are increasingly popular today among homeowners. But if you’re thinking about adding any of these features, it’s important to consider your liability exposure and review your homeowners insurance coverage.

“Liability coverage in your policy can help protect against legal and medical costs if someone is injured on your property or if you accidentally damage someone else’s property,” says Ruiz.

Most policies include three forms of liability coverage:

- Personal liability, which can help with matters like legal costs, settlements, or judgments if you are sued.

- Medical payments, which help cover smaller guest injuries, no matter who’s at fault.

- Property damage, which comes in handy if you or someone in your household causes damage to someone else’s belongings.

However, liability coverage isn’t a one-size-fits-all solution.

“Liability coverage varies by policy, limits, and insurer, and it may not automatically adjust as your lifestyle or property changes,” Ruiz points out. “Certain risks, higher-value assets or frequent entertaining often require higher limits or supplemental coverage to avoid gaps.”

When It’s Time to Review Liability Limits

It’s a good idea to look closely at your existing coverage before the summer season kicks off, especially if you’ve added something new, like a pool or plan to host more often.

“Review your liability coverage any time your home or lifestyle changes in a way that could increase risk, and make sure your policy still matches the level of risk around your home,” advises Swanson.

Many homeowners carry liability limits in the $100,000 to $300,000 range, but that may not be sufficient for your needs. If you frequently entertain or have higher-risk amenities like a , think about adding an , which can provide an extra layer of liability protection beyond your standard homeowners policy.

Ways to Lower Summer Liability Risks at Home

In addition to evaluating and upgrading your coverages, you can decrease liability risks around your property via these tips:

- Inspect stairs, decks, and patios for loose boards, nails, and any trip or fall hazards.

- Secure pool and hot tub areas with fencing, gates, alarms, and/or covers.

- Keep grills at least 10 feet from any structure and keep a fire extinguisher or fire blanket nearby.

- Secure your dog indoors or away from guests when hosting.

- Supervise guests and children closely.

- Ensure that outdoor lighting is sufficient and gates are secure.

- Have a first aid kit nearby.

You want to enjoy entertaining friends and family, bask in the pleasant outdoor climate and relax in the comforts of your yard this summer, without having to worry about someone getting hurt or filing a lawsuit. So take the time to check and improve your while also following best practices for safety, making necessary fixes, and implementing safeguards that can decrease your vulnerability. Remember that a little extra planning, maintenance, and coverage awareness can go a long way.

was produced by and reviewed and distributed by ±¬ÁĎTV.