Furlough vs. layoff vs. termination: What's the difference?

If you're worried about losing your job, you're not alone. Today's economy is tricky. Costs are still rising because of tariffs, and many people are worried that companies will reduce their headcounts to reduce costs or as they transition to AI.

The loss of a job, no matter how it comes about, could make it difficult to keep up with your bills, resulting in debt and necessitating debt relief. But the way you lose a job could have an impact on the benefits you're entitled to afterward. That's why it's important to understand the difference between furlough, layoff, and termination.

In a nutshell, the difference between furlough, layoff, and termination is as follows:

- Furlough is a temporary, unpaid leave from work.

- Layoff is a permanent loss of a job, not due to an employeeŌĆÖs actions.

- Termination is a permanent end to a job, often (though not always) for a specific reason.

ItŌĆÖs important to know what rights you have if any of these things happen to you, so took a closer look at each one.

Key Takeaways:

- Employers sometimes cut labor costs with furloughs, layoffs, or terminations.

- A furlough is an unpaid, temporary interruption in work, but you keep your job and benefits.

- Layoffs and terminations are permanent. Layoffs are usually no-fault, and terminations (firings) are typically for a reason.

Understanding the Legal and Financial Implications of Losing Your Job

Furlough, layoff, and termination all result in the loss of your paycheck. But the difference between layoff and termination, for example, could influence whether you're entitled to collect unemployment benefits.

Generally speaking, if you're furloughed or laid off from your job, you're entitled to unemployment benefits. If you're terminated for cause, you can't collect unemployment. Your state will ask you why you're no longer working.

What makes things tricky is that there's such a thing as a ŌĆ£no-faultŌĆØ termination. From an unemployment standpoint, a layoff and a no-fault termination are virtually the same, in that you should be able to collect benefits as long as you meet your state's requirements.

There's also a difference between voluntary and involuntary termination. Voluntary termination is when you decide to leave your job, whether itŌĆÖs to take a new one, to retire, or for another reason. Involuntary termination is when your employer decides to eliminate your job.

With a voluntary termination, you're not entitled to unemployment benefits. With involuntary termination, you may be eligible for unemployment benefits if it's considered a no-fault termination.

Most U.S. companies operate on an at-will employment basis. This means your employer can terminate your job at any time, as long as itŌĆÖs for a legal reason. (ItŌĆÖs illegal for an employer to terminate your job based on race, religion, sexual orientation, age, or gender, for example.)

The difference between layoff and termination could also be a factor when youŌĆÖre looking for a new job. A layoff may not make it harder to find work again, as you can simply explain in interviews that your job was eliminated through no fault of your own.

Being terminated for cause, on the other hand, could make it harder to get hired again. If you're terminated for cause, be prepared to explain what steps you're taking to avoid ending up in a repeat situation.

What You Need to Know About a Furlough

A furlough, or mandatory suspension from work without pay, is as brief or as long as your employer needs it to be, provided they follow certain rules. If youŌĆÖre furloughed, itŌĆÖs generally because your employer doesn't want to lay you off but also canŌĆÖt keep paying your wages in the near term. While thereŌĆÖs no standard time period for a furlough, theyŌĆÖre usually short.

Here are some things to know about being furloughed.

You shouldnŌĆÖt work without pay

As a furloughed employee, you shouldn't do any work for your employer. According to the Department of Labor, if you answer work-related phone calls or emails or engage in any other work-related tasks, your employer must pay you for the time you worked. This holds true whether youŌĆÖre a salaried or an hourly employee.

You get to keep your benefits

If your employer gives you benefits in addition to your salary, you typically keep them while youŌĆÖre furloughed. So if you depend on your employer for health insurance, retirement accounts, life insurance, or other benefits, you probably wonŌĆÖt lose them during this time. However, you might still be required to contribute toward things like health insurance premiums, despite not getting a paycheck.

ItŌĆÖs also common for employers to offer matching contributions to employee retirement plans. You generally wonŌĆÖt get those matching contributions while youŌĆÖre furloughed, though, because youŌĆÖre not getting paid, and therefore arenŌĆÖt contributing to your retirement plan yourself.

You can seek new employment

If youŌĆÖve been furloughed and are technically still someoneŌĆÖs employee, you can still look for a new job. Many furloughed employees take temporary jobs during their furlough period so they can bring in some income. If your goal is to return to your job, you may want to turn to the gig economy for flexible work in the meantime. Earning at least some money could help you avoid the need for debt solutions.

You can collect unemployment benefits

You can usually collect unemployment benefits as a furloughed employee. The amount youŌĆÖre eligible to receive depends on your wages, as well as your stateŌĆöeach state has a maximum weekly unemployment benefit. If you return to work, your unemployment benefits end.

In some cases, when you're furloughed, your hours and paycheck are reduced, as opposed to being paused completely. In this situation, you may be eligible for partial unemployment benefits. Most states use a formula to reduce unemployment benefits based on how much money you're earning while furloughed and working part-time.

Your employer should communicate with you regularly

Because a furlough is not permanent, your employer should keep you updated on when you may be able to return to work. When your company is ready for you to come back, you usually receive a formal recall notice with a return date.

At that point, you have the right to not return to work (such as if you've found a new job). But if you don't go back to work, you generally stop being eligible for unemployment benefits, since the situation becomes a voluntary termination.

ItŌĆÖs important to manage your finances carefully

Although a furlough may only be temporary, you may end up going weeks or months without a paycheck. ItŌĆÖs important to avoid debt as much as you can during that time.

Aim to reduce your expenses, and if you have an , nowŌĆÖs the time to tap it before charging expenses on a credit card. Furthermore, if youŌĆÖve been furloughed and have an installment loan youŌĆÖre paying off, like a mortgage or personal loan, you may want to see if your lender will let you pause your payments temporarily. You may also be eligible for .

What You Need to Know About a Layoff

In a layoff, youŌĆÖre let go from your job due to no fault of your own. It could be that your companyŌĆÖs needs have changed, and theyŌĆÖre downsizing their staff. Or that money is tight, and your employer needs to cut its headcount. ItŌĆÖs possible to be rehired after a layoff, but itŌĆÖs not something to bank on. Here are some things to know about layoffs.

You should seek unemployment benefits

If youŌĆÖve been laid off, file an unemployment claim as soon as possible in the state where you worked. If you receive severance pay from your employer, you might not be eligible for unemployment benefits right away, but itŌĆÖs still a good idea to file your claim so it gets processed. In some states, no benefits are paid for the first couple of weeks after you file, so get that waiting period started.

You may need to apply for new health insurance

Typically, when youŌĆÖre laid off, you lose your workplace benefits right away, including health insurance. You could , a program that continues your health insurance while youŌĆÖre furloughed or laid off. But typically, you have to pay the portion of your insurance that used to be covered by your employer. That could be quite expensive.

You may be better off finding a more affordable alternative through the Affordable Care Act marketplace (healthcare.gov). Medicaid may also be an option if you qualify based on income. Or you may be able to secure health coverage from a spouseŌĆÖs job.

You need to understand your severance package

Your employer may offer you a severance package when they lay you off. It may be a one-time payment or several payments spaced out over time. Your severance may be based on the length of your employment.

To get paid, you may also have to sign a severance agreement in which you give up certain rights. It could pay to review that agreement with an employment lawyer before you sign it. Your severance package and agreement may be negotiable, so you could end up with better terms.

Even if youŌĆÖre not entitled to severance, itŌĆÖs important to get the details of your layoff in writing in case your unemployment claim is denied. ItŌĆÖs also important to understand what benefits youŌĆÖre entitled to (if any) as part of your layoff, such as being paid for accrued vacation or sick days.

You should know what rights you have

Layoffs often come out of the blue. But depending on the size of your company, your employer may be required to give notice of a layoff.

The Worker Adjustment and Retraining Notification (WARN) Act generally requires companies with 100 or more full-time employees to give proper notice (usually 60 days), particularly for mass layoffs. If your company violates this rule, you may want to speak to an employment attorney.

You should try to leave on good terms

It can be difficult not to take a layoff personally, even when itŌĆÖs clear that you arenŌĆÖt being fired for cause. But one thing you generally donŌĆÖt want to do is express anger toward your employer. You never know when your employerŌĆÖs situation might change and when a job may open up for you, whether itŌĆÖs the one youŌĆÖre losing or a new opportunity. So itŌĆÖs worthwhile to leave on good terms and maintain a professional relationship with your employer even after youŌĆÖre collecting a paycheck. You also might need to ask your employer to be a reference for a future job.

What You Need to Know About Termination

When youŌĆÖre terminated from a job, it typically means youŌĆÖre being let go for cause. However, thatŌĆÖs not always the case. Some companies offer voluntary termination, meaning an employee resigns, usually in exchange for some type of payment. And itŌĆÖs also possible to have a no-fault termination, which is similar to a layoff.

Keep in mind that even though most U.S. employment is at-will, you may have grounds for wrongful termination if you're let go for an illegal reason. That includes:

- Discrimination based on your race, nationality, gender, religion, or age.

- Retaliation for reporting a safety violation or harassment in the workplace.

- Letting you go because you took leave you were entitled to, or filed a workersŌĆÖ compensation claim.

Here are some additional things to know about termination.

DonŌĆÖt expect unemployment benefits

Unemployment benefits are generally available to workers who lose their jobs through no fault of their own. If youŌĆÖre terminated for cause, whether because of issues with your performance or for violating your employerŌĆÖs rules, you usually can't claim unemployment benefits. If you file a claim, your employer will likely contest it and say that you're not entitled.

However, you may be able to argue that you're eligible for unemployment due to ŌĆ£constructive dismissal.ŌĆØ Constructive dismissal is when an employee feels compelled to leave their job because their workplace environment is intolerable. This concept may apply if your workplace or manager was hostile, if your working conditions were unsafe, or if your office was unsanitary.

You may or may not be entitled to severance

If youŌĆÖve been terminated from your job, your employer may still offer you severance benefits. If not, you may be entitled to payment for accrued but unused sick or vacation time. Talk to your human resources representative to learn more.

Whether you're eligible for severance or not, it's important to request documentation detailing the terms of your termination. That includes:

- Your employment end date.

- The status of your final paycheck.

- The reason for your termination in writing.

Prepare to lose your benefits

When youŌĆÖre terminated, you typically lose your workplace benefits. As is the case with being laid off, you may need to find a new source of health insurance. However, you may also be eligible to get coverage under COBRA for a period of time (though the cost means itŌĆÖs often better to consider other options, such as the Affordable Care Act marketplace).

If you have a workplace retirement plan, itŌĆÖs important to understand your options. You may be allowed to keep your money in your existing plan. But even if thatŌĆÖs the case, rolling it into a new retirement plan could be a better option.

Start your job hunt as soon as possible

If youŌĆÖve been terminated, you probably canŌĆÖt get unemployment benefits. That could make it difficult to pay your bills and lead to . You might also blow through your emergency savings quickly without a job.

Look for work as soon as possible. Here are a few job search tips that could help you out.

- Network online. Join professional groups on Facebook and LinkedIn, and make it known that youŌĆÖre in the market for a job in your industry.

- Bolster your skills. The more skills you learn and develop, the more options you may have. You can also consider free courses and certification programs.

- Prepare for interviews. If you were at your most recent job for a while, your interview skills may, understandably, be rusty. Practice in front of a mirror to boost your confidence, or find a friend or family member to do mock interviews with you so you get more comfortable.

How Employers Handle Furloughs, Layoffs, and Terminations

When you're furloughed, laid off, or terminated, you're often called into a meeting with your manager and a representative from your company's human resources department. If it's a mass layoff, you may simply be notified by email.

Your employer should provide you with information that includes:

- The details of a furlough, such as whether your hours are being reduced versus cut completely.

- The nature of your termination, such as whether you're being let go for cause.

- Your final employment date.

- Your final paycheck date.

- What benefits to expect, if any.

- The terms of your severance agreement.

- How to return company property, such as a laptop or cell phone, you use for your job.

If youŌĆÖre being terminated for cause, you may be asked to leave immediately. In that case, you may be escorted by a human resources representative to collect your belongings from your workspace. This may also happen if youŌĆÖre being laid off through no fault of your own and your job is ending right away.

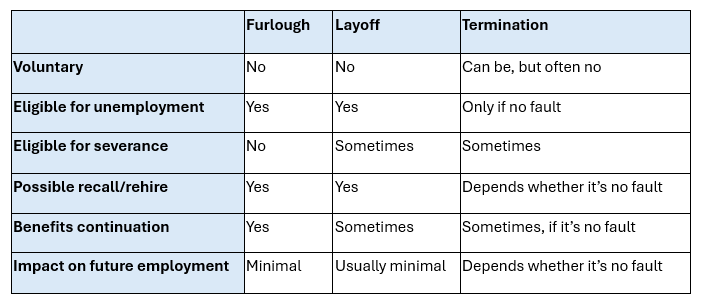

Furlough vs Layoff vs Termination: Key Differences at a Glance

There are a number of key differences between a layoff and a termination, and being furloughed. HereŌĆÖs a summary for easy reference.

ItŌĆÖs important to have a clear understanding of the nature of your job loss, as it could impact your eligibility for benefits, among other things.

Protecting Your Finances After Furlough, Layoff, or Termination

Losing your job, no matter how it happens, could impact your personal finances. If you find yourself out of a job, take these steps.

Assess your emergency fund

See how many weeks or months of bills you can pay out of your savings. If your essential bills come to $2,400 a month and you have $6,000 in savings, you could cover 2.5 months of bills without resorting to debt. And that doesnŌĆÖt include any money you might get from severance or unemployment benefits.

Review your budget

There may be expenses you can cut back on while your job situation is in flux. Comb through your carefully, and try to pinpoint a few bills to reduce. Make sure to prioritize your essential bills like rent, car payment, and food. Consider canceling extras like streaming services temporarily, then resubscribe once your financial situation improves.

Get relief from your debt

It can be hard to pay a mortgage or make minimum payments on your credit cards when youŌĆÖre out of work. Contact your lenders and credit card issuers to see what options you have. You may be able to pause some of your payments or negotiate the terms of a loan to lower your monthly payments. You can also find out how debt relief works if you feel your debts are no longer manageable.

Unfortunately, the loss of a job could lead to more debt, since you may need to rely on credit cards or loans if you're not getting a paycheck. But you may be eligible for debt settlement.

Figure out your most affordable path to health insurance

Losing a job often means losing your health coverage. Going without insurance could result in catastrophic bills if you need surgery or emergency care, so itŌĆÖs important to research your options. Depending on your situation, you may be able to join a spouseŌĆÖs insurance plan at a cost, or you may qualify for subsidies that make an ACA plan more manageable for a time.

Find out if you qualify for government assistance

Depending on your financial situation, you may qualify for government assistance beyond unemployment benefits. You may be eligible for:

- SNAP, which provides food benefits

- Housing assistance

- Medicaid

- Utility bill assistance

Eligibility for these programs generally varies by state.

Losing a job can be a harsh blow, whether itŌĆÖs temporary or permanent, and whether you did something wrong or not. DonŌĆÖt hesitate to turn to family and friends for support as you figure out your next steps.

was produced by and reviewed and distributed by ▒¼┴ŽTV.