7 steps to pay off several bills with debt consolidation

Paying off several bills at once with a debt consolidation loan can help make managing existing debt easier.

By combining multiple bills into a single loan, you pay off several debts at once. Depending on your interest rate, a debt consolidation loan might even help you reduce your total monthly expenses.

However, like most financial decisions, itŌĆÖs important to take it one step at a time. shares a guide to help make it happen:

1. Take inventory of your debt

If you know which debts you want to pay off, use a to add them up. It can help to have an approximate loan amount in mind. If youŌĆÖre not sure, make a list of the balances and interest rates on all your outstanding debt. This can give you a snapshot of which accounts require the most attention. YouŌĆÖll also want to , which can impact your ability to obtain a loan.

2. Check your credit report

If you donŌĆÖt have a current copy of your credit report, there are several ways to ŌĆö youŌĆÖre eligible to receive a free report from all three nationwide consumer credit reporting companies (Equifax, Experian and TransUnion) every 12 months if requested. Applying for the loan does require a hard credit inquiry, which could cause a slight, temporary dip in your credit score. Over the long run, however, a debt consolidation loan can actually improve your credit if you use it to pay down other debts and then make monthly payments on time.

3. Research debt consolidation options

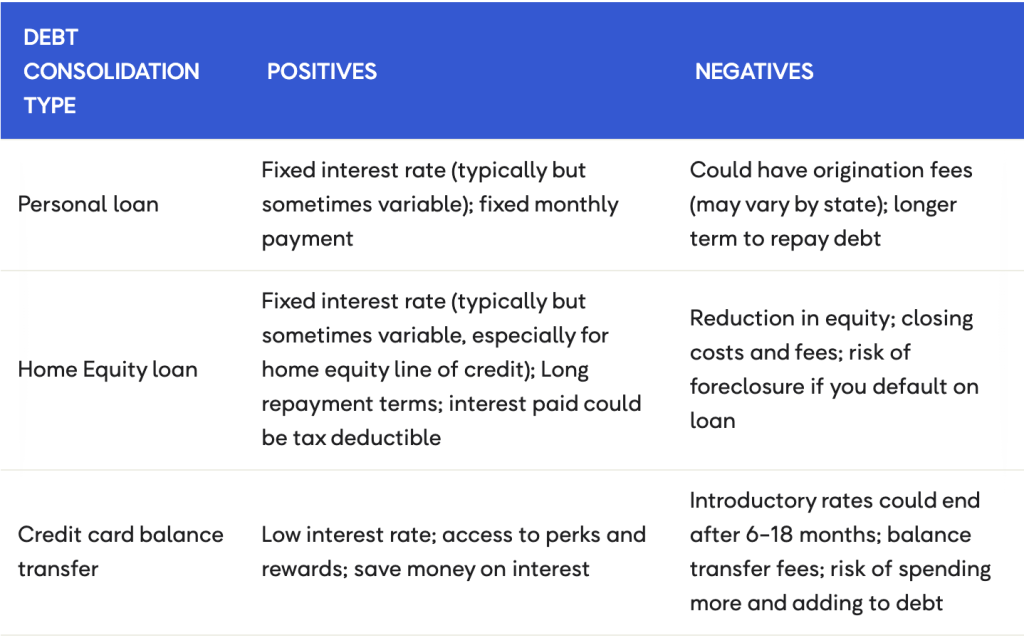

There are to consolidate debt, including personal loans, home equity loans and credit card balance transfers. Make sure to ask yourself the right questions before taking out a loan and take a look at the chart below to help you compare some potential pros and cons of each option:

4. Research debt consolidation companies

Being selective can have its benefits. Look for lenders who not only provide the solutions you need but also have positive customer feedback. For example, check out their online reviews. Next, look up their Better Business Bureau page. You can also ask family and friends if they have a company that they recommend.

5. Get your personal documents ready

Most lenders ask for similar information in their applications. to speed up the process: proof of identity, proof of residence, proof of income and Social Security card.

6. Apply for a debt consolidation loan

Once youŌĆÖre certain a debt consolidation loan is right for you, itŌĆÖs time to see if youŌĆÖre prequalified. If approved, you can move forward with getting your funds. Lenders may provide loan proceeds by check or deposit into a bank account.

If your application is denied, take a look at why it was turned down. You might learn how to improve your chances of getting a loan approved if you choose to apply again in the future.

7. Pay off your debts

Once your funds are available, contact your creditors and pay off the debts you selected. As you pay off each account, be sure to request an official ŌĆ£paid in fullŌĆØ letter from the lender. This letter will certify your zero balance and the date that the outstanding balance was satisfied. In some cases, you may be able to and save money on interest.

Focus on the future

After doing your happy dance, itŌĆÖs important to focus on your new loan. To truly get out of debt, youŌĆÖll need to make your payments in full and on time. If you stick to the plan, youŌĆÖll be on your way to another ŌĆ£paid in fullŌĆØ letter. Once your debt is paid off, be sure to focus on developing healthy financial habits in order to stay debt free.

was produced by and reviewed and distributed by ▒¼┴ŽTV.