What the higher 401(k) and IRA contribution limits for 2026 mean for your retirement strategy

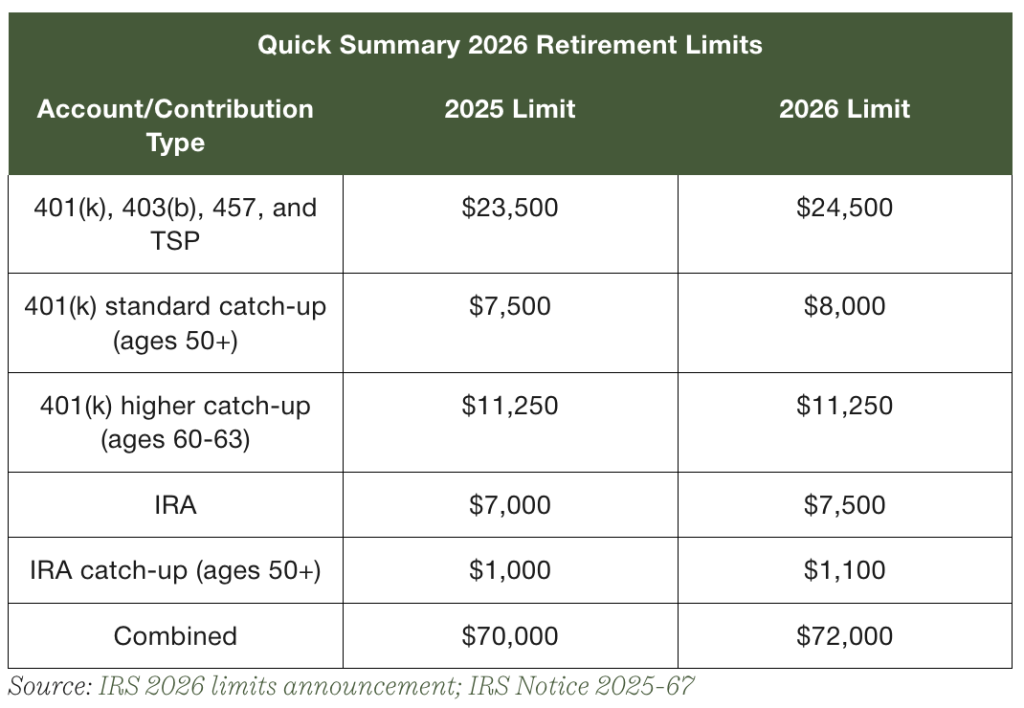

The IRS has you can contribute to your retirement accounts in 2026. You can now contribute up to $24,500 to your 401(k) plan, up from $23,500 in 2025, and up to $7,500 to your individual retirement account (IRA), up from $7,000 in 2025.

These increased limits create more room for tax-advantaged retirement savings in your financial plan. All of this will result in a lower tax burden today, along with more savings in your retirement nest egg years down the road.

Whether youŌĆÖre just getting started saving or are well on your way to reaching your retirement goals, itŌĆÖs important to understand how these new numbers affect you, who benefits the most, and next steps are to consider.

explains how the 2026 increase in contribution limits may affect retirement planning strategies and savings decisions.

2026 Retirement Contribution Limits at a Glance

Why the IRS Raised 401(k) and IRA Limits for 2026

Section 415 of the Internal Revenue Code requires the Secretary of the Treasury to reassess retirement contribution limits every year and adjust them if needed based on cost-of-living increases. In years where the cost of living rises more significantly, so too will your contribution limits.

These increases change how much you can save, but they donŌĆÖt change the basic account framework, including the tax treatment and eligibility rules. Even as the limits change, you can put more money to work in tax-advantaged accounts without having to open new accounts or change your overall savings strategy.

What the 2026 401(k) Contribution Limits Mean in Practice

There are several different pieces to the 2026 401(k) contribution limits, and itŌĆÖs important to understand how each one works and which pieces affect you.

Employee deferral limit

Every employee who has access to a 401(k), 403(b), 457(b), or Thrift Savings Plan . This only applies to your own contribution limits, and it applies to everyone, no matter your age. Employer contributions are separate.

Standard catch-up contribution limit

Once you reach age 50, you can make an additional catch-up contribution of up to $8,000 per year, up from $7,500 the year before. This means that if youŌĆÖre 50 or older, your personal total contribution limit is $32,500.

Higher catch-up contribution limit

Thanks to SECURE 2.0, employees ages 60, 61, 62, and 63 get an even higher catch-up contribution limit. You can now contribute up to $11,250 in addition to the elective deferral, instead of $8,000. As a result, your personal total contribution limit is $35,750.

Total contribution limit

Many employers contribute to their employeesŌĆÖ 401(k) accounts on their behalf, either as matching or nonmatching contributions. The total limit for both employee and employer contributions combined is $72,000 in 2026, not including catch-up contributions.

What the 2026 IRA Contribution Limits Mean

In 2026, the IRS allows you to contribute , up from $7,000 the previous year. These contributions are separate from and in addition to any workplace retirement contributions you make. In addition to the standard contribution, thereŌĆÖs also a catch-up contribution of $1,100 allowed for workers ages 50 and older.

These contribution limits apply to both combined. You can contribute to both accounts in the same year, but your total contributions across the two canŌĆÖt exceed the annual limit.

Can You Contribute to Both a 401(k) and an IRA in 2026?

In most cases, yes, you can contribute to both a 401(k) and an IRA. Contributing to a workplace plan doesnŌĆÖt limit your ability to contribute to an IRA, and vice versa. For example, you could contribute $24,500 to your workplace 401(k), and then another $8,000 to your IRA. And if youŌĆÖre 50 or older, you could make catch-up contributions to both accounts, bringing your total contributions to more than $40,000.

However, workplace coverage could limit your eligibility for certain tax benefits.

How Income Limits Can Change Your IRA Strategy

The IRS places certain income limits on taking advantage of the . If your income is too high, you may be prohibited from deducting your traditional IRA contributions or contributing to a Roth IRA.

Traditional IRA deduction limits

If you or your spouse is covered by a workplace retirement plan, your ability to deduct your traditional IRA contributions may be reduced or eliminated at a certain income level if you have workplace coverage. For single taxpayers, this phase-out happens between $81,000 and $91,000 of income. For married taxpayers, it happens between $129,000 and $149,000 of income.

You can still contribute to the account if your income is higher than the limits, but you wonŌĆÖt receive an upfront deduction.

Roth IRA income limits for 2026

Roth IRA contributions are subject to income phaseout ranges. Once your income surpasses the top limit, you wonŌĆÖt be able to contribute to a Roth IRA. The phase-out range is $153,000 to $168,000 for single filers, and $242,000 to $252,000 for married filers.

What high earners should watch

A higher income, while certainly beneficial in most areas, can limit your direct Roth IRA contributions and the deductibility of your traditional IRA contributions. But that doesnŌĆÖt necessarily mean IRAs are off the table ŌĆö it will just change your strategy.

For example, if your income is too high to deduct your traditional IRA contributions or contribute to a Roth IRA, consider using a backdoor Roth IRA to ensure you still have some tax benefit. You can contribute to a traditional IRA, roll those contributions over into a Roth IRA, and enjoy tax-free withdrawals later on.

Should You Prioritize a 401(k) or an IRA First?

ThereŌĆÖs no universal right answer to whether you should prioritize your 401(k) or IRA, but thereŌĆÖs a general framework that can help you plan your savings.

Start with the employer match

If your employer offers a matching contribution to your 401(k), prioritize contributing enough to earn the full match. For example, your employer might offer to match your contributions at 50% on up to 6% of your salary (a common approach employers take). If you earn $100,000, thatŌĆÖs an employer match of $3,000 if you contribute $6,000 to your account.

When an IRA may come next

Once youŌĆÖve taken advantage of your full employer match, you might consider switching to your IRA before adding more to your 401(k). IRAs typically offer broader investment flexibility. Rather than being limited to those investment options your employer selects, you can choose from anything your broker offers.

Additionally, if your employer only offers pretax retirement savings, opting for an IRA can help you gain exposure to both pretax and Roth tax benefits.

When it makes sense to keep adding to your 401(k)

After maximizing your IRA contributions, or if youŌĆÖre not eligible for a deductible or Roth IRA, continue increasing your 401(k) contributions as much as you can.

401(k) contributions come with the convenience of having the money directly withdrawn from your paycheck before taxes, eliminating an extra step for you. These accounts also have higher contribution limits than IRAs, meaning you can keep saving even once youŌĆÖve hit the IRA contribution limit.

DollarŌĆæcost averaging (DCA) in a 401(k) is the natural effect of contributing a portion of every paycheck to your retirement plan on a regular schedule. Instead of trying to time the market, you automatically invest the same dollar amount (or percentage of pay) every pay period, regardless of whether the market is up or down. When prices are high, your contribution buys fewer shares; when prices are low, it buys more shares. Over time, this can lower your average cost per share and reduce the risk of putting a large sum into the market at the wrong time.

In practice, DCA works especially well in 401(k)s because contributions are systematic, automated, and longŌĆæterm. You donŌĆÖt have to make timing decisions; emotions are taken out of investing, and market volatility becomes your ally rather than something to fear. While dollarŌĆæcost averaging doesnŌĆÖt guarantee higher returns or protect against losses, it helps smooth the ride, encourages consistent saving discipline, and aligns well with the long-term horizons typical of retirement investing.

How Higher 2026 Limits Can Improve Your Retirement Strategy

Increase contributions with each raise

One of the simplest ways to take advantage of higher contribution limits is to raise your contributions whenever your income increases. If you use percentage-based contributions, then this will happen automatically with each raise. But you could also take things one step further and increase your contribution percentage as your income rises.

Use higher limits to build tax diversification

Higher contribution limits create more room to spread your retirement savings across . For example, you can use both pretax and Roth accounts to get exposure to diversified tax benefits ŌĆö one that helps you now and one that will help you later.

Having these different tax benefits can really come in handy during retirement, as youŌĆÖll have more options when designing the ideal withdrawal strategy to help minimize your tax burden.

Coordinate contributions across spouses

Two-income households may be able to expand their retirement savings by coordinating contributions to each spouseŌĆÖs 401(k) plans and IRAs. Each spouse is subject to separate limits, meaning a married couple under age 50 can contribute a combined $49,000 to 401(k)s and $16,000 to IRAs. ThatŌĆÖs $65,000 in tax-advantage savings every year.

Spousal IRAs

A Spousal IRA lets a nonworking or lowerŌĆæearning spouse contribute to an IRA using the working spouseŌĆÖs earned income, if the couple files a joint tax return. Normally, you must have earned income to fund an IRA, but the spousal IRA rule allows each spouse to have their own IRA in their own name, even if only one spouse works.

For 2026, each spouse can contribute up to $7,500, or $8,600 if age 50+, provided the working spouseŌĆÖs earned income is at least equal to the total of both contributions. Spousal IRAs can be traditional or Roth, with the same income limits, deduction rules, and Roth eligibility phaseouts that apply to any IRA. The key advantages are that they double a householdŌĆÖs IRA savings, help protect the nonworking spouseŌĆÖs retirement independence, increase tax diversification (pretax versus Roth), and improve longŌĆæterm planning for retirement income and estate strategy. In short, spousal IRAs are one of the simplest and most underused ways for married couples to build more taxŌĆæadvantaged retirement savings.

Aftertax 401(k) Contributions

Aftertax 401(k) contributions are a special third type of contribution (separate from pretax and Roth) that uses alreadyŌĆætaxed income and allows you to save beyond the normal $24,500 employee deferral limit, up to the overall 401(k) cap ($72,000 in 2026, including employer match). On their own, aftertax contributions are not very attractive because earnings are eventually taxed, but they become extremely powerful when the plan allows inŌĆæplan Roth conversions or inŌĆæservice rollovers.

In that case, the aftertax contributions (and often their minimal earnings) can be quickly converted to Roth, creating whatŌĆÖs known as a ŌĆ£Mega Backdoor Roth,ŌĆØ which effectively lets high earners move tens of thousands of dollars per year into Roth space with no income limits. The result is significantly more taxŌĆæfree growth, better control over future tax brackets and RMDs, and greater flexibility for retirement income and estate planning if the employer plan supports the necessary conversion features.

Real-Life Examples of How Different Savers Might Respond

Real-life examples can help you get an idea of at different points in your career. While these scenarios arenŌĆÖt personalized advice, they can be a good starting point.

Early career saver

Steve is 24 years old and in an entry-level job. He just started contributing to his accounts, and he doesnŌĆÖt earn enough to max out his contributions. However, he sets his contributions high enough to earn his full employer match and plans to slowly increase his contribution percentage as their income rises.

If SteveŌĆÖs employer offers automatic increases, he could increase his withholding by 1% each year, up to a specific limit. With a longer runway, Steve has more time to save, but also more potential for his money to compound.

Given SteveŌĆÖs lower income at this phase in his life, he decides that Roth contributions make the most sense. He has less need for the tax benefit of a tax deduction now, and itŌĆÖs likely his income will be higher in the future, when the tax break might be more helpful.

High-income professional

Jane is a 40-year-old manager who has been with her company for the last decade. Thanks to moving up in the ranks of her career, Jane has more money to invest and is able to max out her 401(k) each year.

However, Jane also runs into some roadblocks because of her income. For example, her income is too high to contribute to a Roth IRA or to deduct her traditional IRA contributions. Instead, Jane decides to talk to her financial advisor about either taking advantage of a nondeductible traditional IRA or using a backdoor Roth IRA to maximize her retirement savings tools.

Age-52 saver

Brandon is an executive who has been contributing to his retirement accounts for decades. Now that heŌĆÖs in his 50s, he is eligible for the for both his 401(k) and IRA, meaning the amount they can contribute each year has increased dramatically.

BrandonŌĆÖs children are graduating from college, meaning heŌĆÖs out of the most expensive phases of raising children, freeing up more money for investing. Between that and his higher income, heŌĆÖs able to prioritize retirement savings to ensure he can retire on time.

Age-61 saver

Rebecca is in her 60s and is thinking more and more about retirement. Thanks to SECURE 2.0, Rebecca is able to contribute even more to her 401(k), and sheŌĆÖs doing just that.

In addition to contributing more, Rebecca is talking to her advisor about her exit plan. SheŌĆÖs running the numbers to make sure sheŌĆÖll have enough money to retire in just a few years, and sheŌĆÖs starting to plan out the right withdrawal strategy in a way that minimizes her tax burden.

Common Mistakes to Avoid

Unfortunately, plenty of people make mistakes with their retirement savings that end up costing them money down the road. Here are a few mistakes to avoid to give you the best chance of success.

- Missing the full employer match: Your employer match is free money from your employer. It can add up thousands of dollars per year, and hundreds of thousands in the long run, especially when you account for compound interest.

- Assuming a 401(k) blocks all IRA contributions: Participating in a workplace retirement plan doesnŌĆÖt prevent you from investing in an IRA, and you could miss out on powerful tax benefits if you donŌĆÖt take advantage of both.

- Ignoring Roth IRA income limits: If your income climbs above the phaseout range for Roth IRA contributions but you havenŌĆÖt changed your contribution approach, you could be on the hook for penalties.

- Overlooking catch-up eligibility: Many savers in their 50s and 60s donŌĆÖt realize they qualify for catch-up contributions, or they donŌĆÖt update their payroll elections to take advantage of them. ThatŌĆÖs thousands of dollars per year in missed contributions.

- Front-loading 401(k) contributions without checking match rules: may sound efficient, but some employers use a per-paycheck matching formula. In this case, you could miss out on the majority of your employerŌĆÖs match for the year.

Action Checklist for 2026

Not sure where to start? HereŌĆÖs an easy checklist you can use to make the most of your 2026 retirement contributions. This isnŌĆÖt a substitute for personalized advice, but can serve as an excellent starting point:

- Review the current payroll deferral percentage. Make sure itŌĆÖs still appropriate given your income, financial goals, and the current contribution limits.

- Check whether you are on track to capture the full employer match. Even if you canŌĆÖt max out your account, make sure youŌĆÖre contributing enough to get your full employer match, and prioritize that over other retirement savings.

- Confirm whether income changes the IRA strategy. Review the Roth and traditional IRA income phase-outs to ensure your income isnŌĆÖt over the limit to maximize the benefits of these accounts.

- Decide on the traditional versus Roth mix. Many people use a mix of both pretax and Roth accounts to diversify their tax benefits, but itŌĆÖs important to determine what works best for you.

- Update automated contributions. If youŌĆÖve set a flat dollar amount rather than a percentage, you may need to manually update your contributions as your income and the contribution limits change.

- Review catch-up eligibility if age 50 or older. Once you turn 50, confirm what the catch-up contribution limits are and how to take advantage of them.

FAQs

What is the 401(k) contribution limit for 2026?

The elective deferral limit for 401(k)s is $24,500 in 2026. The catch-up contribution is $8,000 for those 50 and older, and $11,250 for those ages 60 through 63.

What is the IRA contribution limit for 2026?

The IRA contribution limit is $7,500 in 2026, with an additional $1,100 catch-up contribution allowed for workers ages 50 and older.

Who qualifies for catch-up contributions in 2026?

Anyone age 50 or older qualifies for the standard catch-up contribution, while those ages 60, 61, 62, or 63 may qualify for the higher catch-up contribution in certain workplace plans.

Should I max out my 401(k) first or contribute to an IRA too?

You donŌĆÖt necessarily need to max out your entire 401(k) before contributing to an IRA, but you should contribute at least enough to earn your full employer match. After that, you can compare taxes, fees, investment choices, and flexibility across the two plans to decide which to prioritize next.

Can I contribute to a 401(k) and a Roth IRA in the same year?

Yes, you can contribute to both a 401(k) and a Roth IRA in the same year, as long as your income falls within the limits set by the IRS.

Do employer contributions count toward the 401(k) employee limit?

No, employer contributions donŌĆÖt count toward the 401(k) employee limit. However, there is a combined annual limit that covers both employee and employer contributions.

Conclusion

Higher retirement account limits in 2026 create more room for tax-advantaged saving. ThereŌĆÖs no one right way to make the most of these changes. The best strategy for you depends on your companyŌĆÖs match structure, how much you earn, and how long you have until retirement, among other things.

This information is not intended as a recommendation. The opinions are subject to change at any time and no forecasts can be guaranteed. Investment decisions should always be made based on an investorŌĆÖs specific circumstances. Investing involves risk, including possible loss of principal.

was produced by and reviewed and distributed by ▒¼┴ŽTV.